Moving from the linear to the circular economy is, in theory, simple. In our current model, the linear economy takes, uses, and disposes. In a circular economy, the cycle is to use, reuse, maintain, refurbish, recycle, and compost to avoid waste.

Circular business models (CBMs) are at the forefront of the shift towards a more sustainable and more circular economy.

Adopting circular practices may involve changing a product design to use locally sourced materials, reduce the number of assembly steps, or switch to renewable resources — with the aim of lowering production costs, reducing waste, and sparking innovation. Moving toward a CBM may seem like a lot of effort for little payoff, particularly to small and midsize businesses, but it offers a way to increase sustainability and business opportunity.

Adopting circular practices

A framework and an accompanying tool developed by UK researchers as part of the AICPA and CIMA’s global research programme provide a structured approach to avoid waste, explore modular design, support local communities, rely on renewable energy, and regenerate nature. The tool, named the Circularity Radar, allows management accountants to kick-start a plan and identify the financial and operational challenges ahead. Adopting circular practices not only allows businesses to comply with existing and future regulations but also to unlock substantial long-term cost savings and explore additional financial benefits.

Based on 40 interviews and workshops with retailers, manufacturers, service providers, and industry experts as well as a literature review, we identified a comprehensive set of mechanisms, principles, and ways to achieve sustainability and circularity in retail and associated manufacturing. The framework and tool focus on these sectors, including textiles, furniture, electronics, and household goods. They can also apply to other sectors not specifically mentioned; for example, they might be applicable to the construction or defence sectors.

A critical role for management accountants is mapping sustainability into measurable costs, benefits, and financial impacts. For example, identifying the potential savings from reduced material consumption makes circularity practices financially attractive in the longer term, even if it requires an upfront investment.

The framework and Circularity Radar tool provide valuable insights for management accountants to develop KPIs and integrate these metrics into budgeting, forecasting, and financial reporting processes.

A framework for sustainability and circularity

Achieving circularity in practice requires several elements. The graphic “Framework for Retailers and Manufacturers,” below, has seven interconnected categories: eco-design, sustainable operations, sustainable materials, R terms or strategies (such as reduce, reuse, repair), product stewardship, social aspects, and strategic organisational positioning. Many of these elements are interlinked. For example, eco-design principles include design for disassembly, which makes it easier to dismantle a product for repair, upgrading, remanufacturing, or recycling.

The framework also shows four external factors that influence the way CBMs are implemented: pressure from shareholders and other stakeholders; innovation in technologies, services, and business models; government policies, regulations, laws, and taxes; and customer demand. The framework is flexible, as strategies, implementation, and environments are context-dependent.

The framework highlights the multidimensional approach needed for retailers and manufacturers to transition towards CBMs. It emphasises collaboration, sustainability, innovative design, responsible material sourcing, and the integration of social and operational aspects. Organisations require a high degree of orchestration, and a large part of the discussion will involve the financial costs and benefits associated with new business models.

The Circularity Radar tool

The tool constitutes an early-stage and guided self-assessment exercise that can help businesses evaluate their current situation and potential for improvement through a simple and user-friendly interface. Additionally, the tool’s output can serve as a supplementary resource to support reporting by providing measurable data on how companies perform in terms of environmental and social performance metrics. It helps businesses align their governance practices with circular economy goals, enhancing transparency for stakeholders.

The digital tool can be accessed online or downloaded for local deployment.

Once an initial self-assessment is completed, companies can use the information in the tool to explore additional ways to measure and monitor circularity opportunities through more specific instruments at levels beyond the organisational one, such as departments, products, or their supply chain. Likewise, the assessment results can be used to set specific, measurable targets for circularity that align with both financial objectives and ESG (environmental, social, and governance) goals. Applying the Circularity Radar can create a clear pathway for continuous improvement.

If you have feedback or ideas to improve the Circularity Radar, please contact the research team at r.frei@arts.ac.uk.

The Circularity Radar: Practical application

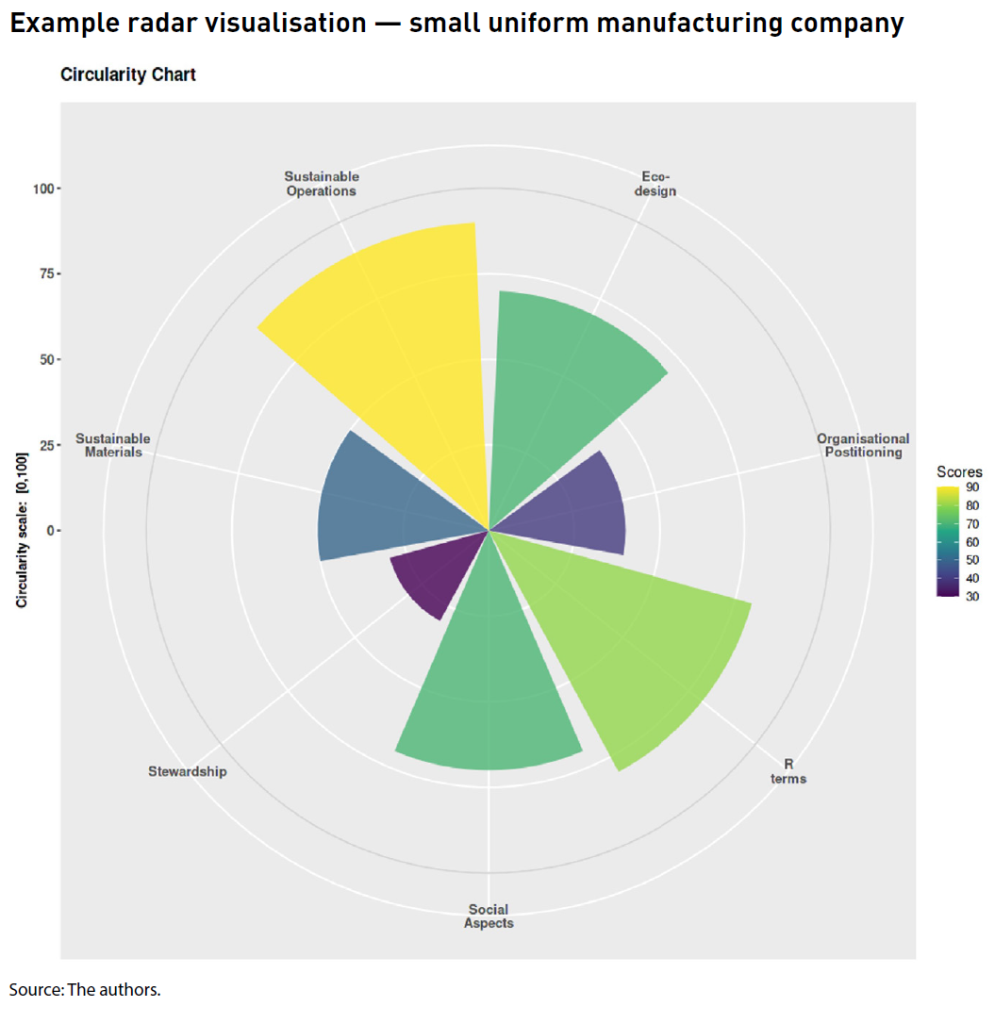

As an illustrative example, let’s consider the case of a small textile company making work uniforms. It is keen to review the extent to which its operations are currently circular and sustainable and identify opportunities for improvement. The company uses the Circularity Radar in a flexible way, whereby it can modify the individual metrics and their weights to suit their case.

For each category, it selects metrics that are meaningful and able to be self-assessed with a value between 0 (no activity) and 100 (perfect implementation). The Circularity Radar then calculates the weighted averages for each category and displays them in a spider web graph. (See the graphic “Example Radar Visualisation — Small Uniform Manufacturing Company,” below.)

The company does very well in terms of the sustainability of its operations. For example, it collects rainwater, uses renewable energy, minimises cut-off waste, and produces close to its main market. It also does well in terms of the R strategies, as it has reduced the number of materials in its products, it refurbishes and resells items that are returned with minor damage, and its products are often easily repairable. These aspects are linked to its reasonably good performance in terms of eco-design, although it could do more to increase its garments’ longevity and long-lasting appeal to consumers. It should also rethink the materials it uses, as many are sourced far away, have a significant carbon footprint, and are often not recycled despite being recyclable.

The company provides good working conditions and requires its suppliers to do the same, supporting employers as well as their families. There is potential for doing more for the welfare of the wider communities.

The two weakest aspects are stewardship and strategic organisational positioning. Once the product is sold, the company does not take responsibility for it. There are no take-back schemes, the company does not offer tailoring or repair services, and it is not involved in textile recycling. It also has not (yet) strategically positioned itself as a company doing business responsibly and sustainably, despite many of its practices being aligned with these values. There is a significant opportunity to change this, with an increasing consumer segment holding companies accountable for their impact.

The Circularity Radar comes with a predefined set of 45 sub-components, but the tool is flexible enough for organisations to add or remove sub-components according to their relevance and applicability. This will enable companies of different sizes, markets, and sectors to adjust the tool to their specific needs and particular business models.

Regina Frei, Ph.D., is a professor of sustainable and circular systems at the University of the Arts London. Danni Zhang, Ph.D., is a lecturer in logistics and operations management at Cardiff Business School. Felipe Merlano, Ph.D., is a research fellow at the University of Surrey. To comment on this article or to suggest an idea for another article, contact Oliver Rowe at Oliver.Rowe@aicpa-cima.com.

LEARNING RESOURCES

Introduction to the European Sustainability Reporting Standards

The European Sustainability Reporting Standards (ESRS) for use by all companies subject to the Corporate Sustainability Reporting Directive (CSRD) are explored for accounting and finance professionals.

COURSE

Oxford Sustainability Reporting and ESG Data Management Programme

COURSE

This programme, developed in partnership with the University of Oxford’s Saïd Business School, empowers mid-level finance and accounting professionals to develop, implement, and enhance sustainability reporting strategies within their organisations.

MEMBER RESOURCE

Article

“4 Actions to Align Sustainability Goals With Digital Transformation”, FM magazine, 11 October 2024