A Mayan prediction of global catastrophe in 2012 made for a thrilling plot in Roland Emmerich’s movie “2012”, with civilisation destroyed by earthquakes, solar flares and volcanic activity.

Judging by the way last year closed out, the Mayans’ cataclysmic myth was wrong, but, some would say, not by much.

The International Monetary Fund (IMF) certainly thinks so. Its World Economic Outlook report states baldly: “The risks are clearly to the downside.”

By October, UK finance directors’ confidence had dropped to the lowest level since two and a half years ago when Lehman Brothers’ collapse was still fresh in minds, according to Deloitte’s CFO Survey. The big supermarket chain Tesco declared that it was facing “the most challenging retail market we have seen for a generation.”

In the US, economic optimism among CPA financial executives registered at a slightly improved but still gloomy 19% as the year wound down. Forty-five percent believed that it was likely that the US would experience a double-dip recession, according to the AICPA Business & Industry Economic Outlook Survey Q4 2011.

Globally, the mood is slightly more buoyant. Even so, the Organization of the Petroleum Exporting Countries (OPEC) has cut its 2012 global economic growth forecast from 3.7% to 3.6%.

The reasons for these jitters are many and varied. The Western banking sector remains in turmoil. Around the world, governments’ finances are out of kilter with one another (either because, like China, they have too much cash or, like the US, the EU and most of the rest, too much debt). Faced with high-level political paralysis, the euro zone is confronting what German Chancellor Angela Merkel has described as “its toughest hour since the second world war.” And from the streets of North Africa to Wall Street, people have expressed their anger in a wave of social-media-fuelled protests about capitalism’s perceived shortcomings.

Whatever else organisations have to deal with, it’s clear that prevailing global economic conditions will be the defining issue in the coming months for organisations of all sizes.

The demise of “business as usual”

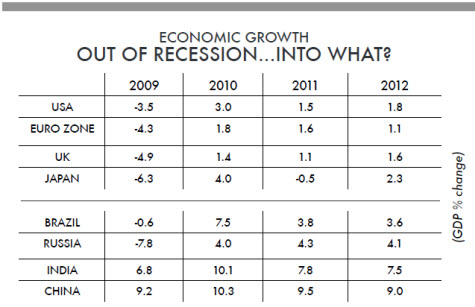

The consensus for 2012 is that the world economy won’t grow by much (see table below). But that target for global growth is made up of a mix of robust emerging economies and sluggish developed ones.

Something fundamental has changed. Within a decade, China is set to become the world’s largest economy. It’s already the biggest market for cars, personal computers and an ever-expanding list of other high-value products. And over the next 20 years, consumption in India will quadruple, according to McKinsey estimates, with the emergence of a middle-class population numbering half a billion. These two countries are no longer emerging; they have well and truly emerged.

“Ongoing globalisation is adding generally to world prosperity, but there are painful adjustments for certain parts of it,” says Bridget Rosewell, economic adviser to the London Assembly and non-executive director at several companies, including the Co-operative Bank and Network Rail in the UK.

“For the old Western economies, there is doom and gloom, but that’s really about them hardening up a bit after going soft in the good years and coming to terms with getting relatively, but not absolutely, poorer,” she explains. “Look east, and the picture is very different. It’s all a question of perspective.”

China is transforming itself and with it the world. It is moving up the value chain, snapping up patents, and has in the process pulled hundreds of millions out of poverty and created new mass markets for Western-style consumer goods.

India is not so far behind in the race to become an economic superpower. Yet despite their impressive growth, the emerging economies won’t enjoy a smooth ride this year.

“Even in China, where a multibillion-dollar health-care investment programme is under way, the government is currently extremely cost-conscious,” says Irelan Tam, FCMA, CGMA, regional finance director for Johnson & Johnson Medical Asia Pacific.

“China won’t get the growth rates it needs to suppress unemployment through its traditional routes because its export markets of the US and Europe are so weak,” adds HSBC’s chief economist Dennis Turner. “It needs to spend internally, and that’s an opportunity for the US and Europe. Companies really need to work out their BRICs strategy in 2012.” (See our guide to transformative drivers below for more on the relationship between East and West).

Accountants’ role

Sleek cars manufactured by BMW, Jaguar and Mercedes enjoy buoyant sales in China, now also General Motors’ biggest market. But even the strongest export drive to China won’t solve the economic woes of Europe and the US. And for businesses in these mature economies, tight financial discipline is the order of the day.

“Businesses that survive through the year will undoubtedly emerge stronger – more efficient, more outward-looking, leaner,” says Norman Green, FCMA, CGMA, former UK finance director at Oracle Corporation and now chief operating officer of Britain’s Conservative Party. “The ones that will do well, domestically or globally, will be flexible in their approach. That’s another area where quick-minded and value-focused accountants can really help them deliver.”

In appointing Will Periam, ACMA, CGMA, as its director of business strategy across Asia, Ford is putting the interdepartmental value of management accountancy into practice. “My job is to harness the existing and imminent growth opportunities in the region, pull every strand of our business together, and map out Ford’s growth plan – from Chinese joint ventures, via relationships with governments, to new product development,” he says.

“Over the years I’ve worked in five countries on four continents for Ford. My training in financial analysis, control and accounting has been relevant in every role I’ve performed – both inside and outside the finance department.” (See “Financial Expertise Across the Business” below for more on the importance of instilling financial expertise across the business).

Periam and his team plan to launch or expand 15 vehicles in China over the next five years, and nine in India.

It is long-term thinking that will distinguish companies struggling through 2012 from those who thrive beyond it, says CIMA technical specialist Peter Simons, ACMA, CGMA.

“The single biggest reason why companies fail is that they don’t address long-recognised, long-term risks, probably because their planning horizons are too short. The rebalancing of the economy with less debt and a smaller public sector, shifting demographics, the rise of more informed consumers and e-enabled competitors, climate change, societal values, limited resources … these all present longer-term challenges to many business models, and they need to be addressed.” (See “Understanding the causes of corporate failure” for details of a new report on the causes of corporate failures.)

“In traditional economic cycles, you eventually come out the other end – recessions end,” Turner says. “But this time, you just can’t assume we’ll return to business as usual. We don’t even really know what ‘usual’ is any more.”

This requires modelling a wider variety of scenarios, with fewer firm assumptions. “We just have to forecast a lot,” says Brenda Morris, CPA, CGMA, the CFO of US fashion retailer Love Culture. “Monitoring all the internal and external drivers is a huge job. With the unexpected shocks we’ve seen, it’s also impossible to anticipate and model for every eventuality. But you can still have a range of models that give you some visibility into different scenarios and plan for the downside – until you can see clearly that you’re in a base-case scenario or better.”

Source: IMF World Economic Outlook September 2011 (2011 and 2012 figures forecast)

The downside risks

The IMF has identified four main downside risks in the global economy this year and warns that any of them could push individual national economies back into recession. They are:

1 Fragile public finances and weak banks in a number of advanced economies.

2 Insufficiently strong policies to address the legacy of the crisis in the major advanced economies.

3 Vulnerabilities in a number of emerging market economies.

4 Volatile commodity prices and geopolitical tensions.

If there’s good news in this list, it’s that these factors have all been in play for a long time and should have been factored into budgets and forecasts for the year. “The big certainty for 2012 is volatility,” stresses economist Bridget Rosewell. “You need to think about how you become more robust to risk. You can never mitigate every eventuality, but you can try to plan for a variety of shocks and insulate yourself from them. Just don’t assume your central forecast is reliable.”

Carol Scott, CPA, CGMA, the AICPA’s vice president for business, industry and government, agrees that, while these global macroeconomic risks can seem remote from operational planning, they must be taken into account. “We can’t be insular any more – the problems with government stability and debt are worldwide,” she says. “And now globalisation has broken down the boundaries, issues arising in Europe or China feed through much more quickly to US businesses, for example.”

CIMA technical specialist Peter Simons, ACMA, CGMA, adds: “We have research that says most companies have responded to this crisis tactically rather than strategically. They have battened down the hatches while they hope for conditions to improve. The credit crunch, originally seen as a short-term liquidity crisis, is now referred to as the debt crisis. It may even signal a second big contraction – as bad as the one in 1929.”

Regulation: A new political weakness?

From the Great Depression to the fall of Enron, one lesson from past economic upheavals and corporate collapses is that they spur increased interest among politicians and regulators in reform.

The European Commission launched in October 2010 a broad discussion on whether audit regulations should be changed to mitigate future financial risks. In late November 2011, the EC proposed regulations that would, if approved, trigger major changes in the relationships between European public companies and their auditors.

The changes include limiting to six years the period that an outside auditing firm can perform audits for a company. A cooling-off period of four years would be imposed before a firm could audit again for the same client. Companies that opt for a voluntary joint audit would be allowed a nine-year window. Audit firms would be prohibited from providing nonaudit consultancy services to their audit clients, and large audit firms would be required to separate audit activities from nonaudit activities. While significant, the package of proposed changes was ratcheted down from measures European financial services commissioner Michel Barnier reportedly favoured.

In the UK, the Office of Fair Trading (OFT) expressed concerns about concentration and barriers to entry in the audit market and referred the question of audit services for large companies in the UK to the national Competition Commission. The commission must issue a decision on the matter within two years.

Meanwhile, the US Public Company Accounting Oversight Board (PCAOB) is debating potential limits on audit firm tenure with public companies, with a particular focus on audit terms of ten years or greater. The regulator will hold a public forum on the issue in March. “Firm rotation would not be cheap for American business,” PCAOB member Daniel Goelzer said when the board issued its concept release, pointing to a report from the US Government Accountability Office, in which large firms estimated that, under rotation, first-year audit costs would increase by 20%.

Separately, the PCAOB proposed amendments to improve audit transparency and is expected to release proposed changes to the auditors’ reporting model by the second quarter.

However, a flagging economy does not necessarily spark calls for ever-tougher regulation. In the US, there have been calls from some in Congress for cost-benefit analysis of any future regulations proposed by the Securities and Exchange Commission (SEC). And in an effort to jump-start job creation, some lawmakers have proposed scaling back certain regulations. Bills introduced in Congress would expand exemptions to internal control assessment requirements under Section 404(b) of the Sarbanes-Oxley Act, the law designed to shore up public confidence in financial reporting.

Meanwhile, in the UK the so-called gold-plating of European regulations remains a popular bogeyman. Within Europe more generally, many complain that rigid employment legislation hurts competitiveness. And even in China, politically motivated regulation also affects market demand and, particularly, transactions conducted for foreign firms.

The Arab Spring, the global wave of Occupy movements and the pace at which euro-zone leaders have been ousted suggests that incumbent governments scarcely have an advantage.

Businesses will also have to adapt to the sea change in the environment they operate in. The best will view this as a chance to seize on unforeseen opportunities in a world where billions can number themselves in the ranks of the middle class and new technologies favour new thinking. And individuals who understand cost leadership, aligning KPIs to outcomes and other staples of management accountancy will have an edge in creating sustainable value.

Accounting for change

The accelerating pace of globalisation continues to push convergence of accounting standards up the regulatory agenda. Will 2012 be the year that finally sees International Financial Reporting Standards (IFRS) become a truly global language? The key, of course, is the US. “The SEC is unlikely to fully adopt IFRS in 2012, but there is lots of interest in a ‘condorsement’ between US Generally Accepted Accounting Principles and IFRS,” explains the AICPA’s Scott.

“Condorsement”? The word was coined by SEC deputy chief accountant Paul Beswick to describe a piecemeal convergence involving the US Financial Accounting Standards Board (FASB) winding up current convergence work and shifting its attention to bringing US standards into line with the established IFRSs. In November, the Financial Accounting Foundation (FAF), parent to the US standard-setter FASB, broadcast in a letter to the SEC its concerns with the condorsement approach and pushed for a stronger role for FASB in the international standard-setting process.

FASB and the International Accounting Standards Board (IASB) are expected to wrap up a multi-year convergence programme in 2012. For US GAAP- and IFRS-reporting accountants, that means significant changes in revenue recognition, lease accounting, insurance contracts and financial instruments.

But the volume and value of accounting standards looks certain to remain on the agenda, particularly for hard-pressed smaller businesses. Financial reporting standards for private entities should also be an issue this year. In the US, the AICPA and others, including members of a panel convened on the topic, are seeking a separate board independent from FASB to set financial reporting standards for private companies. FAF has proposed creating a Private Company Standards Improvement Council to determine whether exceptions or modifications to US GAAP are required to improve standards for private companies.

“We’re disappointed that the FAF has decided not to convene a separate board to work on simpler and more relevant standards for private companies,” says Scott. “It would have been a major step – and we would like to send a strong message that this is an important issue.”

Globally, the introduction of IFRS for SMEs in 2009 offered a solution to at least part of that problem. Adoption should accelerate during the coming months (73 countries have already adopted or announced plans to do so). And even in countries where the formal start date is later (such as the UK, where the Accounting Standards Board has deferred the effective date of its proposed framework until January 1st 2015), finance teams should be looking to prepare prioryear comparatives and learning how changes might affect them.

“The other big news in 2012 should be the development of more integrated reporting,” says CIMA’s reporting specialist Nick Topazio, ACMA, CGMA. “The International Integrated Reporting Council will publish an exposure draft, and we’ll see the first results from the pilot programme as South Africa moves into its second reporting cycle of mandatory integrated reporting.”

In a year when external factors – such as economics and availability of capital – are likely to dominate accountants’ thinking, the focus on long-term sustainability of the business inherent in integrated reporting is more critical than ever.

“Management accountants are good at guiding a business plan – it’s not just about recording activities and presenting historical data,” says Green, the former Oracle UK CFO. “So how well they support investment plans, forward sales initiatives and expansion into new markets is just vital. They need to work with the business holistically.”

On the other side of the Atlantic, Morris, the Love Culture CFO, agrees. “The No. 1 issue for me in 2012 is how we drive sales,” she says. “All my priorities come back to that – whether it’s helping our people become more efficient so they can concentrate on driving sales, or delivering lower costs so we can focus our cash on sales activities.”

So while management accountants the world over should never forget the financial disciplines – and have to step up their forecasting and risk management activities in a world where no region is free from volatility – it will be their success in supporting growth that will define how well they perform in 2012.

Click here to download “Ten transformers” as a table (PDF)

1. Power of transparency

Transformative drivers

Businesses must learn to live with total transparency where anything they do or write may end up being made public. With digital technology changing social attitudes and new legislation opening up corporations’ inner workings to public scrutiny, manipulating public perceptions of a company is becoming difficult, if not impossible. The challenge is to use transparency to corporate advantage and capitalise on living in a world where truth will win out.

What CGMAs bring

Management accountants understand the power and value of information not just to run the company but also to report to external stakeholders. By focusing on providing high-quality financial and nonfinancial information, they ensure that what is revealed to the outside world is integrated and consistent with the intelligence used to run the company.

Risk mitigation considerations

Transparency is closely related to ethics. Accountants in business serve numerous stakeholders and need to understand their responsibilities to all of these stakeholders. This is where professional ethics training and the CIMA and AICPA codes of ethics will help guide efforts. In addition to ethics, management must understand the power and reach of social media. Policies and processes for managing this medium are critical. Ultimately, transparency starts with attitude, and the tone from the top is very important.

2. Financial expertise across the business

Transformative drivers

Smart companies involve their financial people beyond the finance function unit to leverage the power of finance in creating value for the business in a complex global economy and in ensuring that business decisions are grounded in financial reality.

What CGMAs bring

Management accountants can be trusted to provide an objective view of performance and strategic alternatives, thereby guiding critical business decisions and driving strong performance. They are uniquely placed to provide the relevant management information the board needs to understand how the business model works and to marshal nonfinancial data on environmental impacts and other factors key to integrated reporting.

Risk mitigation considerations

The strengths of finance and operations professionals are complementary. Moving finance professionals into business partnering roles will create value for the organisation. Management should look for these opportunities. Start with specific projects. Over time, the partnering will happen naturally.

3. Success factors for sustainable businesses

Transformative drivers

Cost leadership, innovation and a repeatable business model that a company can apply to new products and markets over and over again are among the factors that will decide which companies succeed and which don’t. Culture and leadership are important, too, with those weighing long-term and short-term considerations equally proving more capable of building sustainable businesses than those eager for short-term gains.

What CGMAs bring

Management accountants understand how the different parts of the business need to come together to make money and create value. They add value by supporting and driving the right decisions in all areas of the organisation to achieve sustainable success for the business by helping their colleagues to understand key value drivers, costs, risks and opportunities.

Risk mitigation considerations

A culture that develops its people and welcomes creative thinking will have an edge. Having strong management and leadership training programmes will help. Learning never stops, and companies that encourage ongoing learning and development will have people that can drive business success. Developing a strategic mind-set among management and an understanding of sustainable business concepts will pay dividends for years to come.

4. Hidden value

Transformative drivers

The power of the financial markets is forcing many mainstream businesses into damaging short-termism. The prevailing culture of financialisation places little or no value on many of the factors that make companies great, including a clear mission, expert processes and know-how, or a motivated workforce.

What CGMAs bring

Management accountants have an understanding and experience of business that goes beyond the financials. They focus on the organisation’s future prospects as well as past performance and use a wide range of information in addition to financial information to measure, manage and report performance.

Risk mitigation considerations

Strategic planning should be an ongoing process. Introducing concepts from CGMA resources on strategy and planning, specifically planning for the intermediate and long term should be an integral part of the process. In addition, planning for disruptive challenges and opportunities should be part of the foundation of building the plan.

5. Ascent of Asia

Transformative drivers

Economic power is shifting fast, with countries such as China and India moving up the value chain more into high technology. The war for talent has become far more intense in Asia than in the US or Europe. China is able to make big foreign acquisitions globally, but rises in wage rates are starting to erode its competitive edge in manufacturing, and some observers predict that Western companies will start to repatriate jobs. Luxury global brands are finding markets in the East. Meanwhile, there is a scramble to find supply chains that do not involve China.

What CGMAs bring

All businesses, regardless of location, strive for long-term sustainable success. To achieve this, they need a resilient business model and the ability to deal effectively with the risks and opportunities of a changing environment. The management accountant is the highly skilled finance professional who meets the needs of business by enabling the right strategic and operational decisions to be made, appropriately funded and effectively implemented.

Risk mitigation considerations

Studying the company’s supply chain, manufacturing and customer footprints should be part of strategic and risk management processes. In addition to identifying risks, the process will identify future opportunities for the business. How will shifting global economic power affect the current business model and future plans? In a rapidly changing, interconnected world, risk management planning should include threats presented by shifting global economic power.

6. Credit crunch / economic instability

Transformative drivers

The sovereign debt crisis has sparked massive uncertainty in the West, threatening a recession, and is having a dramatic impact for the world economy as a whole. It has exposed a lack of global political leadership in the euro zone and Washington, raising fears of “a lost decade” for the developed world’s economies. Real incomes are falling in much of the developed world, making selling into consumer markets tough. In countries with high state spending, the public sector is also bearing the brunt of the cuts, forcing countries to reassess their social welfare models.

What CGMAs bring

Management accountants bring a strategic perspective; they are trained in scanning changes in the external environment and understanding the risk and opportunities that these will create for the organisation’s business model. Management accountants also bring invaluable skills to other sectors, including the public sector, particularly in the areas of performance management and cost control. They can provide invaluable support to policymakers in maximising value for money from tax revenues.

Risk mitigation considerations

Uncertainty in the world economy has increased the risk premium in certain regions. This should be considered in future investment analyses. The concepts of scenario planning are important in this environment. Integrating volatility and uncertainty into the planning process will help businesses respond more rapidly to unexpected events. Strengthening the balance sheet and developing an open, close working partnership with capital providers will help companies respond to adverse changes in economic conditions and take advantage of new opportunities as they arise.

7. Accounting changes

Transformative drivers

With much of the world requiring or allowing the use of IFRS by listed companies, the US entered 2012 undecided, though a vote by the Securities and Exchange Commission is expected before year’s end and the US and international standard-setters continue to hash out converged rules for key areas such as leasing and revenue recognition. Mexico will require adoption of international standards for all listed entities starting in 2012. Japan is set to make a decision regarding its mandatory use of IFRS in 2012. Meanwhile, India missed its deadline for IFRS implementation in 2011 and has yet to set a new one.

What CGMAs bring

Management accountants are trained to monitor, oversee and report on all performance, including financial performance. They are therefore conversant with compliance requirements for financial reporting and are subject to high professional and ethical standards. In so doing, they support the board in fulfilling its compliance requirements for reporting.

Risk mitigation considerations

Boards should make sure management is focused on upcoming changes, including completion of major accounting convergence projects and possible moves to IFRS. Teams should be assembled to follow the progress of these projects and the status of decisions and should assess how the changes would affect financial statements and the resources necessary for implementation.

8. Regulation

Transformative drivers

The fallout from the financial crisis has increased calls for tougher regulation. Both the European Commission and the US Public Company Accounting Oversight Board are scrutinising potential changes to audit policies – such as mandatory rotation of audit firms – that could affect listed companies. Responding to calls from the G20 finance ministers, the EU is also looking for means to improve the corporate governance framework for European companies. The US’s Dodd-Frank Wall Street Reform and Consumer Protection Act spawned a host of regulatory issues for businesses. Meanwhile, the IRS has continued forward on the required disclosure of uncertain tax positions.

What CGMAs bring

Management accountants are qualified to have an understanding of business well beyond financial accounting. They balance both a compliance and strategic perspective, so that while they ensure that their business complies with appropriate regulation at minimum cost, they will also be looking to identify any possible strategic opportunities that may arise. They provide the right information to the board to ensure that regulatory requirements are understood and met effectively.

Risk mitigation considerations

This is also a board-level issue. How will regulatory changes affect the company? Who is in charge of assuring that changes are implemented? Is tax reform on the horizon? The finance organisation should be front and centre in managing these issues, and the board of directors should assure that management is responding adequately to the changing regulatory environment.

9. Cloud computing

Transformative drivers

The ability to access applications, data, servers and storage capacity over the internet promises to continue transforming how business is done. Cloud computing options are allowing small businesses to enter new markets and compete with much bigger players. Companies of all sizes can serve clients and hire staff worldwide without having to travel or open local offices. Look for the cloud to grow bigger in 2012, as analyst firm Gartner says Oracle, IBM and SAP all have major cloud initiatives that will debut during the next two years. In addition, security will remain the top cloud concern.

What CGMAs bring

Management accountants have the training to analyse the potential impact of major innovations such as cloud computing, and to support the business in making strategic decisions in relation to managing the associated risks and opportunities. Management accountants are trained to transform data into meaningful insights that will create value for the business. As cloud computing renders all organisations informationintense at low cost, this skill is more relevant than ever to ensure that business does not drown in data.

Risk mitigation considerations

Cloud computing and other developing technologies such as mobile apps have the potential to reduce costs and increase productivity, but they also come with new security issues. Mobile apps have the potential to transform how management receives information. Taking advantage of opportunities presented by new technology requires strong project management leadership and skills.

10. Disruptive technologies

Transformative drivers

Traditional business models are under renewed assault from disruptive technologies such as 3D printing, biotechnology and tablet computers. Upstart companies can more easily break into existing markets. The traditional “customer-pays” revenue model is also being eroded, with information becoming ubiquitous and free.

For a quick roundup of technology trends likely to shape business in 2012, including data analytics, cloud computing, mobile devices, tablet computers and security risks, read “A transformative year: Technology, everywhere.”

What CGMAs bring

Management accountants understand how the business as a whole needs to come together to create a resilient and profitable business model. Their core cost accounting skills are well suited to analysing new revenue models such as “freemium” (a free basic service with paid-for advanced options) that are fast gaining ground.

Risk mitigation considerations

It begins with understanding risks and opportunities inherent in disruptive technologies. How could disruptive technologies affect your business model? Responding to disruptive technologies should be a core element of a company’s strategic planning process. In addition, management should understand that planning for disruptive technologies is an important component of building a sustainable business.